2015 Remedy (McCloud) FAQs

Your 2015 Remedy (McCloud) questions answered

Your 2015 Remedy (McCloud) questions answered

The 2015 Public Service Pension Scheme reforms included a policy of transitional protection. This meant members closest to retirement stayed in their Principal Civil Service Pension Scheme (PCSPS - classic, classic plus, premium and nuvos) as they had the least amount of time to prepare for the changes.

The Court of Appeal (McCloud Judgement) later found this policy to be discriminatory against younger members in some schemes. Following the ruling the Government confirmed that it would take steps to address the discrimination in all affected public service schemes.

Since the McCloud Judgment the Government has been working on ways to address the discrimination.

The Government consulted between July and October 2020 to gather views on proposals to remove the discrimination. In February 2021, the Government announced the implementation of a Deferred Choice Underpin (DCU) which will allow eligible members to make a choice when they retire, between Principal Civil Service Pension Scheme (PCSPS - classic, classic plus, premium and nuvos) or alpha scheme benefits for the remedy period (1 April 2015 to 31 March 2022).

The Government cannot simply place all members back into the PCSPS scheme without allowing them to access their reformed alpha scheme benefits, because some members are better off in the reformed scheme.

The powers in the Act to make scheme regulations can be used for the various purposes listed throughout the Act. These include for example the process by which a member can make a choice or “election” to receive new scheme benefits, for interest to be paid to a member or scheme on any amounts owed to or by the scheme, to make provision for pension credit members, to make provision for members to receive remediable service statements, to provide for members who have made additional voluntary contributions and for members who have already benefited from an immediate detriment remedy.

Where it is particularly important that scheme regulations are consistent, the Act will require them to be made in line with Treasury Directions. The powers to make scheme regulations are explained in the Delegated Powers Memorandum prepared by HM Treasury for the Delegated Powers and Regulatory Reform Committee.

Following the introduction of the Act, the Government intends that the provisions for the deferred choice underpin will be implemented by 1 October 2023, or earlier where schemes are able to implement legislative change and processes ahead of that date.

The other proposal set out in the consultation was called an ‘immediate choice’ which would allow members to choose which pension scheme benefits they would prefer to take for the remedy period between 2015 and 2022 soon after the point at which schemes implemented the changes.

While this approach would have resolved the issue sooner and provided individuals with more certainty around pension benefits, it would have placed higher risk on the member. This is because they would be basing their choice around assumptions on their future careers, health, retirement and other factors, rather than the facts and known circumstances that will apply at the point of retirement. This would have meant some members may have been much more likely to have chosen the scheme benefits that did not turn out to be best for them.

The Public Service Pensions (Exercise of Powers, Compensation and Information) Directions 2022 were made on 14th December 2022 and came into force on 19th December 2022.

This is in line with the normal use of Treasury and Department of Finance directions in this way, for example directions in relation to scheme valuations, or for increasing public service pensioners’ Guaranteed Minimum Pensions when they would not otherwise be increased.

The Directions set out to schemes how they should exercise the various powers to make regulations in the Public Service Pensions & Judicial Offices Act 2022 (PSP&JOA 2022).

They ensure that, where Treasury ministers (or in relation to Northern Ireland, the Department of Finance) consider that a consistent approach is necessary or desirable, the Treasury (or Department of Finance) may give directions to schemes. Other departments are responsible for preparing and laying scheme regulations.

This allows schemes to make regulations that work best for them, while ensuring that where a particular outcome is desirable, it is achieved.

Together with changes being made through tax regulations using the powers in the Finance Act 2022 and scheme regulations made under the Act, the PSP&JO Act will provide a remedy for all those affected by the discrimination identified by the Court of Appeal.

This remedy will apply equally to claimants in the employment tribunal and non-claimants and there is no need to make a claim to the employment tribunal to benefit from the changes.

The remedy is intended to put scheme members back into the same financial position as if the discrimination had not occurred. This includes provisions to allow schemes to provide compensation for financial losses where members can demonstrate they would previously have taken a different course of action were it not for the discrimination. If members feel they have suffered additional losses this would need to be taken up through the normal channels.

The remedy is intended to put scheme members back into the same financial position as if the discrimination had not occurred and will apply equally to eligible members irrespective of whether they have lodged a claim in the Employment Tribunal. We are not able to comment on ongoing litigation.

No. The discrimination identified by the courts relates to the different treatment applied to members who were in service on 31 March 2012 and still in service on 31 March 2015.

New entrants to the Civil Service who were enrolled into alpha when they joined are not affected by the Court’s ruling. If you had previous public sector pension scheme service prior to joining the Civil Service Pension Scheme, you could also be in scope for 2015 Remedy (McCloud) if your service across both schemes spanned 31 March 2012.

Individuals that meet the following criteria are in scope of the changes:

Yes. All members who were subject to the discrimination will be within scope of any changes made to schemes, irrespective of their status.

No, members do not need to submit a legal claim to receive any pension changes addressing the discrimination.

The Government has committed to applying any changes across the main public service pension schemes and so both claimants and non-claimants who are eligible members will receive the pension changes.

The differences between PCSPS and alpha mean that the set of benefits that is best for you depends on your personal circumstances and preferences. Therefore, the Government is providing you with a choice, to ensure you can choose which scheme benefits are better for you.

1 April 2015 is the date when alpha was introduced, and 31 March 2022 was the point at which the Principal Civil Service Pension Scheme (PCSPS - classic, classic plus, premium and nuvos) was closed to future accrual.

To address the discrimination identified by the courts, eligible members who were moved to the reformed pension scheme (alpha) in 2015 (or later if they had tapered protection) have been moved back into their Legacy pension scheme for the period during which the discrimination occurred, between 1 April 2015 and 31 March 2022.

When members, or members who were originally protected, near retirement, they will receive a choice of which pension scheme benefits they would prefer to take for the period. This is called a ‘deferred choice’.

The choice will be between the member’s Legacy (classic, classic plus, premium and nuvos) pension scheme benefits and their reformed pension scheme benefits.

By deferring the choice until shortly before retirement, it allows individuals to make their choice of which pension scheme benefits are better for them, based on facts and known circumstances as opposed to assumptions on their future career, health, retirement and other factors. The level of both pension scheme benefits will be known at retirement.

For those pensioners who are already receiving benefits relating to the period of discrimination between 2015 and 2022 there will be an immediate choice as soon as practicable once the necessary provisions are in place.

In the case of Civil Service Pension Scheme members, the PCSPS schemes are classic, classic plus, premium and nuvos and the reformed scheme is alpha.

The main differences between the PCSPS and reformed schemes are transition into career average pension schemes from final salary schemes and an increase in normal pension age.

The change to career average means members’ pensions are now calculated on their average salary throughout their career as opposed to their final salary.

The reformed scheme was designed to make public service pensions more affordable and sustainable for the future, while still ensuring public servants received appropriate pension provision at retirement.

The reforms created a fairer system. The move from (mostly) final salary to career average pension means that members accrue pension at a typically higher annual rate based on their average salary. Although some members are better off in their PCSPS scheme, the reformed scheme is more beneficial for others, particularly many lower paid members.

You will be given a choice for how you would like your benefits to be calculated for the Remedy period.

We provide free Pension Power training sessions which you can book onto, the sessions include information about alpha if you wish to learn more about how your pension savings will grow under your new scheme.

The Civil Service Pension website is where all of the current and up to date information is housed on 2015 Remedy (McCloud) along with these helpful FAQs. We are working through the impacts to those members who are affected. As soon as we know how you are impacted, we will tell you what it means for you and what action needs to be taken.

By 31 March 2025 retired members will receive a Remediable Service Statement (RSS) in the post, providing them with their Immediate Choice options for both Legacy (classic, classic plus, premium and nuvos) and Reformed scheme alpha. You will receive a key choice illustration document and additional supporting information to help you decide on the benefits you wish to receive for your service within the Remedy period. You have 12 months to make the choice (from the date of letter) and you will be asked to submit your choice to us online however, if you are unable to do this you can submit your choice by post, via the form provided in your immediate choice pack.

The Government accepts that members affected by immediate detriment have an entitlement to be treated as a member of their legacy scheme for the remedy period if they wish.

However, giving effect to this entitlement before legislation is implemented would create complex issues, particularly where there are interactions with the tax system. Instead processing cases from 1 October when scheme regulations take effect will ensure a consistent approach and mitigate the risk of adverse tax impacts for members.

Where members retire before the deferred choice is implemented in their pension scheme, they will initially receive benefits from their current scheme.

They will then be given a choice of benefits for the remedy period as quickly as possible after that and any increased entitlement will be backdated.

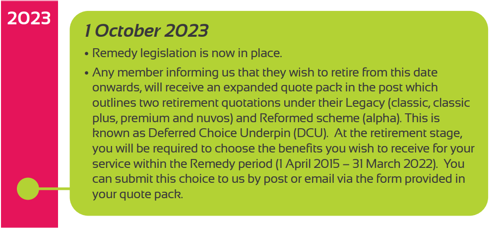

No. There are still detailed changes that need to be made to scheme regulations. These will be made using the powers in the Public Service Pensions & Judicial Offices Act 2022 (PSP&JOA 2022) and need to be in force by 1 October 2023 at the latest.

There are also some situations where changes to pension rights due to the McCloud remedy produce disproportionate tax results that cannot be resolved through powers provided in the PSP&JOA 2022. Therefore, the Government will also be making changes to tax legislation to ensure that the remedy can be implemented smoothly. HMRC consulted on the first set of tax regulations from December 2022 to January 2023; these regulations were subsequently made and laid on 6 February 2023. Further tax regulations will be consulted upon, and finalised, ahead of implementation of the remedy.

The Government has legislated through the Public Service Pensions & Judicial Offices Act (PSP&JOA) to implement a deferred choice underpin within schemes. All eligible members will be treated equally and will be able to choose to receive pension scheme benefits from either scheme at the point benefits become payable. Where necessary, payments will be backdated.

Schemes made prospective regulations in 2022 to bring into effect the closure of all legacy schemes on 31 March 2022 and move members to the reformed scheme. These ensure members are placed in an equal position from this point onwards.

Schemes are consulting on retrospective scheme regulations which will ensure that the detail necessary for the remedy to be implemented in each affected scheme is in place. All schemes will have these regulations in place by 1 October 2023.

These regulations will be used for the various purposes listed throughout the Act, including the process by which a member can make a choice or “election” to receive new scheme benefits, for interest to be paid to a member or scheme on any amounts owed to or by the scheme, to make provision for pension credit members, to make provision for members to receive remediable service statements, to provide for members who have made additional voluntary contributions and for members who have already benefited from an immediate detriment remedy.

Where the changes legislated for through the Act produce disproportionate tax results that cannot be resolved through powers provided in the PSP&JOA 2022, further changes, in the form of tax regulations, will be made using provisions contained in the Finance Act that received Royal Assent on 24 February 2022. HMRC consulted on the first set of tax regulations from December 2022 to January 2023; these regulations were subsequently made and laid on 6 February 2023. Further tax regulations will be consulted upon, and finalised, in the coming months.

In the case of civil service pension scheme members the Legacy schemes are classic, classic plus, premium and nuvos and the reformed scheme is alpha.

Members who received tapered protection in 2015, or would have received such protection but for the provision that unlawfully excluded younger members from transitional protection, will be offered a choice of whether to receive Legacy or reformed scheme benefits in relation to any continuous service between 1 April 2015 and 31 March 2022.

This will remove the discrimination that arose between older members who were subject to transitional protection and younger members who were not.

Members who have retired before the DCU is implemented on 1 October 2023 and have a period of relevant service between 1 April 2015 and 31 March 2022, will retire on their ‘as is’ benefits. At some point after 1 October 2023 these members will be offered a choice; the choice will be retrospective and backdated to the point that payment of pension benefits began.

The remedy attempts to put people in the right position directly; but sometimes it cannot. Where this happens, compensation may be payable in specific cases.

Compensation payments may be made to pension scheme members via application as a result of overpaid tax charges and where this cannot be repaid directly by HMRC. Where contributions have also been overpaid, schemes will provide direct compensation to members. These overpayments would have happened unintentionally through the remedy of the discrimination.

If you have a break in service of five years or more and rejoin the alpha scheme when you return, you won’t be eligible to retain a final salary link from the legacy scheme all the way through to retirement.

Only members included in an ET are subject to any awards and findings made by the Court. The Public Service Pensions and Judicial Offices (PSPJO) Act 2022 provides the legislative framework to allow for all public service schemes to address the discrimination identified by the Court. Scheme specific Regulations introduced allow the government's remedy to be implemented from 1 October 2023.

The Remedy is designed to put all scheme members who were affected by the discrimination, into the same position by removing the discrimination and allowing members the choice of pension benefits they wish to receive for the Remedy period.

There are provisions for schemes to allow compensation for out of pocket expenses in certain circumstances, if they consider the costs result from the discrimination. Details of this and how to apply will be released in due course.

Should you wish to remain updated on the latest Remedy information, the best place to visit is the Civil Service Pensions website which can be accessed by using the following link:

https://www.civilservicepensionscheme.org.uk/your-pension/2015-remedy/

A Contingent Decision is a decision taken by a member, that would have been different had it not been for the discrimination identified by the courts. The decision will relate to their membership of the Civil Service Pension Scheme (CSPS) during the Remedy Period, 1 April 2015 to 31 March 2022.

Members can apply to have their Contingent Decision assessed by the scheme to determine if it can be accepted. This application process is necessary as specific criteria must be met.

At present, the only Contingent Decision you can apply for is to buy back opted out service. This means you are;

We will open applications for other types of Contingent Decisions at a later date agreed by the Scheme Manager.

You could apply to buy back service from 1 April 2015 to 31 March 2022 if you opted out between 12 March 2012 and 28 February 2022, and the reason you opted out was in response to the discrimination identified by the courts.

If your application is successful, your opted-out service can be bought back for all qualifying service built up from 1 April 2015 to 31 March 2022. Your service will be reckonable in your Legacy scheme.

Eligibility summary:

No. If you joined one of the Partnership schemes you are not classed as an opt out member. The applications process for those members who joined a Partnership scheme will open at a later date.

The Remedy Opt Out Member Contributions Estimator is a tool designed to help members understand the potential costs involved in buying back opted-out service. It's important you complete this process before proceeding with your application.

To ensure the information input into the Remedy Opt Out Member Contributions Estimator is as accurate as possible, you'll need;

If you don't have the necessary information, you can contact your employer/previous employer for the necessary details.

You'll be required to supply evidence to support your application. You can supply whatever evidence you feel supports your application in the best way. Some examples of evidence may be:

IMPORTANT: If you don't supply evidence, there's an increased risk that your application will be declined.

Civil Service Pensions

PO Box 2017

Liverpool

L69 2BU

We'll issue you with the below documents:

We may need to engage with your employer/previous employer(s) to obtain additional information to calculate your outstanding contributions and generate these documents. We aim to have these documents completed and issued to you as soon as possible following the issue of your final decision letter.

Once in receipt of your Acceptance Form, we will process your request, reinstate your service record and collect the outstanding contributions owed. We will send confirmation once this has been completed. You will have 12 months to decide and send back your Acceptance Form.

If your application is rejected, we'll provide you with details to explain the reason(s) for this. You can then choose to accept this decision, or you can appeal against the decision. Further information will be sent to you.

You’ll also have the right of appeal to The Pensions Ombudsman.

You can apply on behalf of a member if you have Power of Attorney (POA) or are legally acting on their behalf.

You can also apply if you're making decisions on behalf of a deceased member.

If you're applying on behalf of someone else, you must provide a copy of the relevant documentation showing you have legal power to act on their behalf. This could be, but not limited to Grant of Probate, a valid Will, Letters of Administration or Power of Attorney.

We’ll publish details of the Contingent Decision application process on our website once it is available. It will be open to all members who are in-scope of 2015 Remedy (McCloud), including those that have left or retired from the Civil Service. All Contingent Decision applicants will be asked to provide evidence on the basis of the original decision, to show it resulted from the age discrimination identified by the McCloud judgment. As we cannot guarantee that an application will be successful, please don’t make any decisions about your pension based on an assumption that an application will be agreed.

If a future Contingent Decision application is agreed, you will be provided with information about how the scheme proposes to adjust your pension, and whether there are any costs to be accounted for e.g. additional contributions to be paid where a period of opted-out service is being reinstated. You will have the chance to decide whether you wish to proceed at this stage.

This is in line with the Government's consultation response: https://www.gov.uk/government/consultations/public-service-pension-schemes.

Alongside the public consultation, the Government announced that the pause of the cost control mechanism had been lifted.

By taking into account the increased value of public service pensions as a result of the ‘McCloud remedy’, scheme cost control valuation outcomes showed greater costs than otherwise would have been expected. More detail on this can be found on this page.

The vast majority of contribution rates changed on 1 April 2015 to become the same across all the Civil Service Defined Benefit pension schemes. Therefore, you would have paid the same contribution rate regardless of which scheme you were participating in, and so we don’t expect to refund contributions.

You aren’t due a refund of your contributions as the contribution rates in all of the Civil Service pension schemes (other than partnership) are the same.

If you retired on ill health between 01 April 2015 and 31 March 2022 and are eligible for the 2015 Remedy (McCloud), you will be reassessed for Ill Health Retirement (IHR) under the alternative scheme, either PCSPS or alpha depending on your circumstances.

This is to understand whether any member who applied for ill health retirement during that period would have been eligible for ill health benefits in the alternative pension scheme.

The reassessment will not affect your original ill health application.

Once the reassessment is completed, we will be writing out to the relevant members to advise the next steps in due course.

You can also visit the following webpage for more information.

If you are affected by the 2015 Remedy and were refused Ill Health Retirement (IHR), after a medical assessment by the Scheme Medical Advisor (Health Assured), between 1 April 2015 and 30 June 2017, please note the following information.

In response to the McCloud judgment, we will shortly begin reassessing those members who were refused IHR, following a medical assessment by the Scheme Medical Advisor (Health Assured). This is to determine whether those who applied for IHR under their old pension scheme, would have qualified for ill health benefits under the alternative pension scheme. If you meet the above criteria, please visit Ill Health Retirement for members affected by Remedy - Civil Service Pension Scheme to determine if you have the option to request a reassessment.

Please contact MyCSP here to register your interest and provide your contact details. When contacting us, be sure to select 'Planning for retirement' and then ‘Ill health retirement' on the contact form, to request a reassessment.

Existing beneficiaries of eligible members will be contacted with a choice of whether to retain the benefits they currently receive or choose the benefits available under the alternative scheme.

In most cases the choice between benefits will fall to the late member’s surviving spouse or partner. If there are children also in receipt of a survivor pension, and the decision maker lives in a separate household to the child, any decision taken will not affect the child’s pension. Where the child and decision maker live in the same household, the usual rules around total survivor benefits payable will apply.

Yes. If your spouse was affected by the age discrimination your pension will be reviewed and we will write to you once we’re in a position to confirm how the changes will affect you. Please check the website for updates.

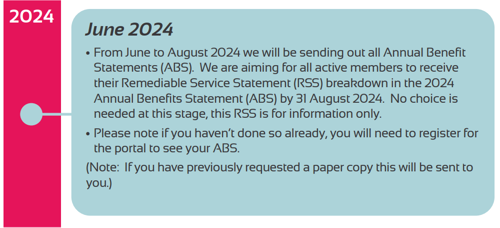

Members who would usually expect to receive a PSS and are impacted by the 2015 Remedy (McCloud) will not receive a 2022/23 statement just yet, instead it will be issued by 6 October 2024. This is with the exception of members who were fully protected and did not join alpha until 1 April 2022.

On 1 October 2023, the pensionable service of eligible Remedy affected members was 'rolled back' into their’ relevant Legacy scheme (classic, classic plus, premium or nuvos) for the Remedy period (1 April 2015 to 31 March 2022) which will likely result in changes to members’ Pension Input Amounts (PIA).

We are recalculating the PIAs for all members affected by rollback. A PSS for the Remedy period and for the 2022/23 tax year will be issued to those members by 6 October 2024 and will replace any previously issued PSS.

For members who were protected and did not join alpha until 1 April 2022, there is no change to their Remedy period of service as they have not needed to be rolled back into their Legacy scheme. The PSS for eligible protected members, for the 2022/2023 tax year, has been issued as normal.

Members who exceed their Annual Allowance or earn over £100,000 and are not affected by the 2015 Remedy (McCloud), were issued with a 2022/23 PSS as normal.

Eligibility criteria

Each year we issue a PSS to members who meet one or more of the following criteria:

-They have exceeded the Annual Allowance limit of £40,000* (for 2022/23).

-They earn over £100,000.

-They have requested a PSS.

The deadline for a PSS to be issued is normally 6 October each year.

Members who have been rolled back into their Legacy section from alpha, should not include information relating to an Annual Allowance tax charge on their 2022/23 Self-Assessment return.

For those who need to complete Self-Assessment this year, they do not need to include any Annual Allowance tax charge deriving from their impacted public sector pension scheme. When the PSS is issued, this can be reported through an electronic form at www.gov.uk/guidance/calculate-your-public-service-pension-adjustment.

If due to the Remedy, there are changes to the amount of Annual Allowance for earlier years this should also be reported to HMRC using the electronic form, previously submitted Self-Assessment tax returns should not be amended. However, members will only be able to use this service once they have received their 2022/23 PSS and any revised PSS for an earlier tax year.

Please note that this doesn’t mean that members won't have to complete Self-Assessment, to deal with and pay any other tax charges, for which they are individually liable for by 31 January 2024.

The deadline for Remedy affected members to ask the scheme to pay all, or part, of an Annual Allowance tax charge (a scheme pays election) for 2022/23 has been extended to 6 July 2025, unless you were a pensioner on 1 October 2023 in which case the deadline is 8 July 2027.

For members affected by the 2015 Remedy (McCloud), who had alpha service between 1 April 2015 and 31 March 2022, a PSS issued now will not conform to the law. This is because it doesn’t present accurate values of pension savings growth in either alpha or the Principal Civil Service Pension Scheme (PCSPS) (classic, classic plus, premium or nuvos).

MyCSP will recalculate the PIAs for all members affected by rollback, and a PSS for the Remedy period and for the 2022/23 tax year will be issued to each affected member by 6 October 2024 if they are eligible to receive one.

Eligibility criteria

Each year we issue a PSS to members who meet one or more of the following criteria:

-They have exceeded the Annual Allowance limit of £40,000* (for 2022/23).

-They earn over £100,000.

-They have requested a PSS.

The deadline for a PSS to be issued is normally 6 October each year.

For members affected by the 2015 Remedy (McCloud), who had alpha service between 1 April 2015 and 31 March 2022, a PSS issued now will not conform to the law. This is because it doesn’t present accurate values of pension savings growth in either alpha or the Principal Civil Service Pension Scheme (PCSPS) (classic, classic plus, premium or nuvos). MyCSP will recalculate the PIAs for all members affected by rollback, and a PSS for the Remedy period and for the 2022/23 tax year will be issued to each affected member by 6 October 2024 if they are eligible to receive one.

Eligibility criteria

Each year we issue a PSS to members who meet one or more of the following criteria:

-They have exceeded the Annual Allowance limit of £40,000* (for 2022/23).

-They earn over £100,000.

-They have requested a PSS.

The deadline for a PSS to be issued is normally 6 October each year.

The vast majority of members will see no changes to their tax position.

In some cases, individuals may be due an Annual Allowance tax charge refund or pay higher Annual Allowance charges, but typically only where their projected pension at retirement has increased. Similarly, a small number of members that are already in receipt of their pension may need to pay additional Lifetime Allowance charges when the total value of their pension has increased.

Where a member’s tax liability does increase, this will not exceed what they would have paid had they always been a member of the scheme they are moving into or receiving equivalent benefits.

The legal process will take into account the tax implications and HMRC are working alongside HM Treasury and the Civil Service Pensions team to make sure that this important issue is taken into account.

As the pension policy proposals are still being finalised, it is not possible at this stage to say how they will interact with the tax system.

Therefore, it would be helpful if you would keep tax paperwork relating from April 2015 onwards. This would include:

Most members will see no changes to their tax position as a result of the remedy or will receive a refund as a result of the remedy.

In the instances where your tax liability does increase, in the vast majority of cases this will reflect an increase in value of your pension benefits received.

Most members will see no changes to their tax position as a result of the remedy; if a member has overpaid tax, they will receive a refund for in scope tax years and compensation for out of scope years.

In the instances where a member’s tax liability does increase, in the vast majority of cases this will reflect an increase in value of their pension benefits.

Given that the remedy relies largely on a member’s choice, which will differ depending on their circumstances, it is not possible to give a meaningful estimate of the number of tax corrections needed as a result of the remedy.

However, the majority of members will see no changes to their tax position or will receive a refund as a result of the remedy.

In the instances where a member’s tax liability does increase, in the vast majority of cases this will reflect an increase in value of their pension benefits.

The tax system will in most instances work in the usual way and follow the new pension rights accrued from the remedy taking effect. There are some situations where changes to pension rights due to the McCloud remedy produce disproportionate tax results that cannot be resolved through powers provided in the Public Service Pensions & Judicial Offices Act 2022 (PSP&JOA 2022).

Therefore, the Government will be making changes to tax legislation, using provisions contained in the Finance Act that received Royal Assent on 24 February 2022, to ensure that the remedy can be implemented smoothly.

HMRC consulted on the first set of tax regulations from December 2022 to January 2023; these regulations were subsequently made and laid on 6 February 2023. Further tax regulations will be consulted upon, and finalised, ahead of implementation of the remedy.

When individuals are moved back into their legacy schemes, they will be legally entitled to receive legacy benefits which have accrued during remedy period years – and that needs to be reflected in their tax treatment.

In the majority of cases this is likely to result in a refund of overpaid tax and/or compensation (in the form of increased pension benefits, or a cash sum), rather than additional tax being due. If an active or deferred (someone who is no longer building up entitlement) member then chooses new scheme benefits when they retire, those benefits will be adjusted at that point, and tax applied as appropriate – not with retrospective effect.

Where the choice of new scheme benefits which arrive all at one point means a higher tax bill that year than if the individual had chosen to keep legacy benefits for remedy period years, the Government will intervene. This is because the design of the remedy could trigger a disproportionately high AA charge.

Where possible, the Government and schemes will take proportionate steps to minimise the administrative burden on members. Although ultimately, decisions made by members will be individual choices.

There will also be further guidance to complement existing HMRC guidance and schemes’ processes which are already in place to help individuals with their tax affairs.

Schemes will also be able to provide compensation where a member has incurred reasonable additional costs as a result of an agent, i.e. where receipts or invoices can be provided by a tax adviser or accountant, who helped to resubmit information to HMRC.

In practice, most individuals will not have to correct their position, either through the tax system or by claiming compensation.

For those that do, the Government has worked hard to remove additional burdens that arise from addressing the discrimination.

Where possible, the Government and schemes will take proportionate steps to minimise the administrative burden on members, but it will not be possible to completely remove individuals from this process in all cases.

If as a result of the remedy an individual has less tax to pay, they may be able to claim a repayment of overpaid tax from HMRC. If they are unable to get a repayment through the tax system, the Act allows them to claim compensation (in the form of increased pension benefits or a cash sum).

The Government acknowledges the need to provide clear and accurate information to members going through this process, to enable them to take the required actions. There will be material to support individuals through this process, including guidance and calculators. Schemes will also be able to provide compensation where a member has incurred reasonable additional costs as a result of an agent, i.e. a tax adviser or accountant, having to resubmit information to HMRC.

This is a unique set of circumstances that the Government is addressing.

The existing legislation and scheme rules covering public service pensions were not created with a view to making retrospective pension provision. So the changes made by the Public Service Pensions & Judicial Offices Act 2022 (PSP&JOA 2022) and other legislation are not straightforward but, as far as individuals are concerned, the complex changes are being made ‘under the bonnet’.

Individuals will have a choice to make, and they will have the necessary information available to them when they come to do so. The majority will be provided with a simple choice between two options.

However, for more complicated scenarios, the Government acknowledges the need to provide clear and accurate communication and information to members going through this process. There will also be further guidance to complement the existing HMRC guidance and schemes’ processes which are already in place to help individuals with their tax affairs.

Schemes will be able to provide compensation where a member has incurred reasonable additional costs as a result of an agent, i.e. a tax adviser or accountant, having to resubmit information to HMRC as a result of the remedy.

The PSP&JOA 2022 contains the core remedy, as well as the bespoke remedy measures for the Judicial Pension Scheme and Local Government Pension Scheme and was published on 20 July 2021. It sets out what the core remedy will mean for member’s contributions, benefits, pension payments and compensation.

Some elements of the Act concerning contributions, timing of changes to pension rights, and deeming provisions regarding which schemes are making or receiving payments, have been included to ensure proportionate and reasonable tax outcomes, in line with policy set out in the consultation and published response document.

The tax system will in most instances work in the usual way and follow the new pension rights accrued from the remedy taking effect.

There are some situations where changes to pension rights due to the McCloud remedy produce disproportionate tax results that cannot be resolved through powers provided in the PSP&JOA 2022. Therefore, the Government will be making changes to tax legislation, using provisions contained in the Finance Act that received Royal Assent on 24 February 2022, to lay tax regulations, which will ensure that the remedy can be implemented smoothly. HMRC consulted on the first set of tax regulations from December 2022 to January 2023; these regulations were subsequently made and laid on 6 February 2023. Further tax regulations will be consulted upon, and finalised, in the coming months.

The HMRC Digital Service

Your pension tax position in remedy period years may be affected due to rollback. HMRC have introduced a new digital calculator and interactive guidance, to help you identify whether you need to take any action. This can be found here:

If you’ve any new annual allowance charges or changes to your annual allowance charges, due to rollback, you can use the service to:

The digital service will also apply to other tax charges such as lifetime allowance charges and unauthorised payments charges.

Our records show that you are impacted by 2015 Remedy (2015 Remedy (McCloud) - Civil Service Pension Scheme).

As a result, your benefits were ‘rolled back’ (reverted) into your Legacy scheme (classic, classic plus, premium or nuvos) for the Remedy period (1 April 2015 – 31 March 2022) and your Pension Input Amounts (PIAs) have been recalculated during that period. They have also been calculated for 2022/2023 as you were not provided with these previously.

Schemes are required to provide members with Pension Input Amounts (PIAs), which show the increase or growth in the value of benefits over a set period.

See the Remedy PSS website page for information and support video explaining your Remedy PSS

Your revised PIA(s) have been recalculated based on Legacy service up to 31/03/2022 and alpha service from 01/04/2022.

No, your PIA will only be recalculated once. At retirement you will be given two options in respect of your Remedy service, and we will calculate your PIA for the year of your retirement based on which option calculates the lower PIA, irrespective of the option you take. If you chose the Legacy scheme, your PIA would remain unchanged.

All members need to calculate whether a charge is due, and whether any past charges have changed. You can do this using the HMRC Public Service Pension Adjustment calculator.

HM Revenue & Customs (HMRC) have developed an online service to help you calculate these changes to your pension tax charges. It'll tell you whether you’re due a refund of tax you’ve previously paid, or if you’ve got new tax charges to pay. It'll also tell you if neither is the case, in which case you won’t need to take any further action. The service walks you through a series of steps and automatically transmits your information to your pension scheme, where necessary.

Details of your total taxable income.

The Pension Input Amounts on your Remedy PSS.

Details of your personal allowance from 2015/2016 to 2022/2023. You can find this on your ‘P60’ for each year. You can also find the last 5 years of these in the HMRC app. If you can’t find the information, contact your employer.

Self-Assessment tax returns, if you filed any.

If you’re due a tax refund for 2019/2020 to 2021/2022 (inclusive), you’ll be able to provide your bank details via the service so HMRC can pay it to you directly. If you are due a refund for earlier years, or need to reduce a past Scheme Pays charge, your scheme will compensate you. If you have a tax charge to pay, you'll have the option of paying this through your pension scheme out of your accrued benefits, rather than out of your own pocket - this is known as ‘Scheme Pays.’

Members shouldn't need to complete Scheme Pays quote requests forms, as HMRC will provide all the required information to MyCSP to adjust an existing Scheme Pays debit, or to set up a new debit.

You should not report any new tax charges for the tax years 2015/2016 – 2022/2023 through Self-Assessment, you need to use the calculate your public service pension adjustment service.

How the public service pensions remedy affects your pension

You can contact HMRC’s specialist team at: publicservicepensionsremedy@hmrc.gov.uk or on 0300 123 1079 (select option 1) for help with information about your taxable income, Self-Assessment returns or personal allowance for previous years.

Yes, you can still retire before you have acted regarding any outstanding tax charges. You can still use Scheme Pays after you have retired, for any additional tax charge, and any necessary adjustments to your pension can be made after you have applied for this.

Previous PSSs were issued based on the data held at the time. You may have queried some of the data that caused you to breach previously, and this has now been corrected. Our records do, however, still show that you received a PSS during the Remedy period.

If you didn't have a tax charge previously and this remains the case, you don't need to take any further action.

You could have overpaid a tax charge if you previously paid an Annual Allowance Tax Charge in the Remedy period and, in the same year:

If you’ve worked out you have overpaid tax charges in the Remedy period, you should submit your inputs into the Public Service Pension Adjustment Calculator to report it to HMRC.

HMRC will assess your pension inputs and provide information to the scheme regarding any compensation due.

Once you have entered your Pension Input Amounts (PIAs) using the HMRC Pension Adjustment Service calculator, it will show you if there are any tax charges relating to the period. If there are, you must ensure that you submit your inputs to report this to HMRC.

You should then follow HMRC guidelines for paying any tax due.

You can pay your Annual Allowance Tax Charge (AATC) by cash directly to HMRC or you can elect to use Scheme Pays.

There are many scenarios, and some will require further data to be provided from the ceding scheme, in particular where the transfer included new scheme remediable service from the ceding scheme (we will use data based on Legacy only in the Remedy period).

If we have all the data we need, then we will treat any remediable service in Civil Service Pension Scheme (CSPS) as Legacy and any transferred in remediable service as Legacy for PIA purposes. However, if there are elements in the transfer relating to Member Voluntary Contributions (MVCs) (e.g., added pension) then these will have to adopt the same treatment as alpha added pension, i.e., the value remains there for PIA purposes.

These relate specifically to transfers in and added pension. The rights from these remain in alpha (and count in the years following) until the point of conversion which will take place in the future, at a date which is yet to be determined.

Once my added pension/transfer in etc has been converted to PCSPS will my PIA need recalculating again?

No, but the converted benefits will count in subsequent PIAs as Legacy.

If no, what if it would have reduced my tax charge as PIA is now lower once converted?

It wouldn’t have, as the conversion is not retrospective.

If you’ve worked out you have overpaid tax charges in the Remedy period, you should submit your inputs into the Public Service Pension Adjustment Calculator to report it to HMRC.

HMRC will assess your pension inputs and provide information to the scheme regarding any compensation due.

If I have data changes that cause previous PIA to be recalculated after the conversion, what basis will my PIA be re-calculated on?

Your revised Remedy PIA was based on the data held at the time and the latest PIA supersedes this.

If you are due to receive a Pensions Savings Statement (PSS) for the 2023/2024 tax year, you should already have been sent it separately. There are some PSS that have been delayed due to some members not yet having received their Remedy PSS. In these cases your PSS will be sent to you separately, after your Remedy Pension Savings Statement (Remedy PSS) has been issued.

What you will need to do in relation to your 2023/2024 PSS is different to your Remedy PSS, and you can find out more about this by visiting the 2023/2024 Pensions Savings Statement page.

The information and support we have made available via the Remedy PSS webpages, along with guidance that HMRC provides as part of its Public Service Pension Adjustment Service, will help you to assess your tax position for the period covered by the Remedy PSS.

If you need additional help in assessing your tax position you may choose to consult a financial professional. You can apply for a reimbursement for the cost of this advice, up to a maximum of £500, if you meet the criteria.

We will reimburse you for such a fee if the following applies:

Please note that if you ask us to reimburse your fees you must provide us with copies of invoices or receipts as evidence of the costs you incurred.

If you want to know more about reimbursement of fees and the points above apply to you, please email us on pss@mycsp.co.uk to begin your claim. If you have any questions, please include them in your email and we’ll get back to you.

These will be offset against any new tax charge. If you no longer have a charge, you could be due compensation and the HMRC will inform you if this is the case.

Out of scope years (now called Compensation Period) - 2015-2016, 2016-2017, 2017-2018, 2018-2019

In scope years (now called Tax Administration Framework) - 2019-2020, 2020-2021, 2021-2022

You may notice that some years prior to 2015 have Pension Input Periods (PIPs) are based on the calendar year and that for 2015/16 there are figures for two Pension Input Amounts (PIAs) listed for two PIPs. This is because HMRC changed Pension Input Periods to match the tax year (6 April to 5 April) from 6 April 2016 onwards. Prior to this change, Pension Input Periods counted toward the tax year in which they ended. For example, the Pension Input Period running from 1 January 2013 - 31 December 2013 ended in tax year 2013/14 and so counts toward that tax year.

When you come to use the HMRC calculator, you don’t need to worry about what time period the Pension Input Period was, the left hand ‘Year’ column corresponds with the fields you’ll be asked to input the figures in that row into the calculator . For the 2015/2016 year, you’ll notice figures for two Pension Input Periods and you’ll find that the HMRC calculator has two corresponding fields to enable you to input both Pension Input Amount figures provided.

The Civil Service Pension Scheme has engaged with HM Revenue & Customs (HMRC) and agreed the following guidance:

Who is affected:

Action you have to take if you think you will have an Annual Allowance charge in 2023/24:

Action you have to take if you think you will not have an Annual Allowance charge in 2023/24

How to estimate the amount saved towards your pension in excess of the Annual Allowance

Please note the following when making the calculations:

Correcting your provisional Self-Assessment figure

When members retire, they receive a choice of which pension scheme benefits they would prefer to take for the Remedy period. This is called a ‘deferred choice’.

To address the discrimination identified by the Courts, eligible members who were moved to alpha in 2015 (or later if they had tapered protection) have been moved back into the Principal Civil Service Pension Scheme (PCSPS - classic, classic plus, premium and nuvos) for the period during which the discrimination occurred, between 1 April 2015 and 31 March 2022 (the remedy period).

The choice is between PCSPS and alpha pension scheme benefits.

By deferring the choice until shortly before retirement, it allows individuals to make their choice of which pension scheme benefits are better for them, based on facts and known circumstances as opposed to assumptions on their future career, health, retirement, and other factors.

You need to choose whichever option is best for you and your personal circumstances. MyCSP are unable to provide advice on what option is best for a member. If you need financial advice, you can contact an Independent Financial Adviser.

Yes, your pension benefits will be paid in accordance with your decision.

No, you need to consider the option carefully before making your decision. The decision cannot be changed and will be paid in accordance with your decision. If you need financial advice, you can contact an Independent Financial Adviser. MyCSP are unable to provide any advice.

Yes, you can defer claiming your alpha pension to a later date. Please advise us in writing if you wish to do this when you return your claim form.

Classic pension is a final salary scheme which means that although you are not accruing pension the final value is still based on current pensionable earnings. Pensionable pay is taken from the date that you retire, looking backwards. If you were in classic, classic plus or premium benefits are being calculated on the most up to date pay figures.

There are a number of different elements to take into account, including annual pension, lump sum and death benefits. In reference to lump sum we will have provided you with the maximum and minimum position to help you make a decision. If you feel unable to make a decision, you can seek advice from an Independent Financial Adviser. MyCSP are unable to provide any advice.

Because you have transferred benefits from another Public Service Pension Scheme into your Civil Service Pension, your benefits were transferred-in under 'Club’ arrangements. The transfer Club is for members who move between ‘Club’ schemes allowing them to transfer pension benefits on special terms. Generally, benefits transferred between Club schemes retain similar value in the new scheme. Because your transfer-in was made during the Remedy period, your previous scheme will need to send us revised calculations so we can offer you the correct 2015 Remedy (McCloud) choices. We may not yet have received the revised/alternative transferred-in calculation from your previous scheme.

We understand that you will want to see your benefits put into payment quickly and efficiently, so we will calculate your retirement quote, using your Legacy scheme (classic, classic plus, premium or nuvos) benefits but excluding the transferred-in part. The benefits resulting from the Club transfer-in will be calculated under the terms of the scheme they were transferred into, potentially alpha and not Legacy.

Once we have the revised calculations from your previous scheme you will receive an Immediate Choice Remediable Service Statement (RSS) and supporting information. This will enable you to make your Remedy choice.

The choice which you eventually make, will be made retrospectively so it will be backdated to the date your pension came into payment, and we will pay any arrears due to you.

Yes you can. Partial retirement enables you to reduce your hours or salary and take some or all of your pension and continue working at the same time. You can also decide how much pension and tax-free lump sum you want to take.

If you're affected by the 2015 Remedy and this is the first time you are taking partial retirement, you can use the Partial Retirement Illustrator tool to give you an idea of the effect partial retirement might have on your benefits. You can use this tool if at least some of the benefits you have built up are affected by the 2015 Remedy.

The Illustrator provides a basic illustration of your projected benefits at partial and full retirement from both your PCSPS (the legacy scheme) and alpha. The Illustrator will also provide a comparison between the Deferred Choice benefits at partial and full retirement. You can find out more about partial retirement if you are affected by the 2015 Remedy [link to landing page for CSP partial retirement if affected by the 2015 Remedy]

You can also read more about partial retirement from the Civil Service in our guide

When members retire, they receive a choice of which pension scheme benefits they would prefer to take for the Remedy period. This is called a ‘deferred choice’.

To address the discrimination identified by the Courts, eligible members who were moved to alpha in 2015 (or later if they had tapered protection) have been moved back into the Principal Civil Service Pension Scheme (PCSPS - classic, classic plus, premium and nuvos) for the period during which the discrimination occurred, between 1 April 2015 and 31 March 2022 (the remedy period).

The choice is between PCSPS and alpha pension scheme benefits.

By deferring the choice until shortly before retirement, it allows individuals to make their choice of which pension scheme benefits are better for them, based on facts and known circumstances as opposed to assumptions on their future career, health, retirement, and other factors.

Active Remedy members, who have taken Partial Retirement and already made their Remedy decision, will receive a single ABS based on the benefits accrued during Reemployment (and any remaining benefits not taken at the time) under the Remedy Option made on Partial Retirement.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

Added Pension which was purchased and commenced in alpha during the Remedy Period (1 April 2015 – 31 March 2022) will be shown in this statement as alpha Added Pension. However, before claiming your benefits, this will also be converted into PCSPS Added Pension and will be shown in your statements as alpha pension.

Added Pension you started to purchase in PCSPS during the Remedy Period (1 April 2015 – 31 March 2022) will be shown in this statement as PCSPS Added pension. However, before claiming your benefits, this will also be converted into alpha Added pension and will be shown in your statements as PCSPS pension.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

Some members (5% of those due to receive an RSS) will not receive their 2025 RSS (made up of two ABS; Legacy ABS and Alternative Scheme Option ABS). However, they will still receive a Legacy ABS by 30 September.

This applies to members affected by Remedy with a Deferred Choice Underpin (DCU) and who:

For members impacted due to their purchase of EPA/EEPA, your Legacy ABS will only show the part of your EPA/EEPA purchased after the Remedy period. The part purchased during the Remedy period will form your alternative scheme option which will be provided at the time of retirement and will also be included in future RSS.

When a member takes their pension, they will have a choice between i) Legacy Pension, with their member EPA/EEPA contributions converted into Legacy scheme Added Pension, or alternatively a refund of their EPA/EEPA member contributions OR ii) alpha EPA/EEPA pension for the Remedy period.

A small number of members (0.4% of those eligible for an ABS) will not receive a 2025 ABS due to the issues outlined above, which cannot be resolved in time for the 2025 ABS distribution.

We have reported this to the pensions regulator and apologise for any inconvenience.

Please note; if you are planning to retire, this will not impact your retirement. You will receive your Remedy retirement quotation, and you can follow the normal retirement process.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme

Transfers into alpha during the Remedy Period (1 April 2015 – 31 March 2022), or after 31 March 2022 from another Club scheme subject to Remedy, will be shown in this statement as alpha pension. However, before claiming your benefits, these transfers will also be converted into PCSPS Pension and will be shown in your statements as alpha pension.

Transfers into PCSPS during the Remedy Period (1 April 2015 – 31 March 2022) or after 31 March 2022 from another Club scheme subject to Remedy, will be shown in this statement as PCSPS pension. However, before claiming your benefits, these transfers will also be converted into alpha pension and will be shown in your statements as PCSPS pension.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

As Divorce Debits, implemented on or after 1st April 2015, need to be assessed and potentially recalculated to reflect the effects of Remedy, we are unable to issue a Legacy ABS or RSS (made up of two ABS; Legacy ABS and Alternative Scheme Option ABS) at this time.

Please note; if you are planning to retire, this will not impact your retirement. You will receive your Remedy retirement quotation, and you can follow the normal retirement process.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

Your scheme pays debit may need to be updated due to the Remedy changes. Whether a revision is required depends on an HMRC assessment. As a result, your RSS (made up of two ABS), will only include your Scheme Pays debits once the HMRC assessment is complete and any revision required has been calculated. If we have received confirmation from HMRC that your tax charges have changed prior to the statement being issued, this will reflect in your statement.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

Members who took Partial Retirement during the Remedy period, including Remedy benefits, will receive an Immediate Choice Remediable Service Statement (RSS). Therefore, your ABS is based on your pre-Remedy Principal Civil Service Pension Scheme (PCSPS) and alpha benefits. After you make your immediate choice, any benefits paid at final retirement will match your selected option.

For more information regarding 2015 Remedy McCloud visit 2015 Remedy (McCloud) - Civil Service Pension Scheme.

If you don't know your length of service, you can find this from the payroll system or a previous ABS. If you're still unable to obtain your length of service then you should use your best estimate.

As a result of 2015 Remedy (McCloud), new legislation requires all Public Service Schemes to issue remedy eligible members with a deferred Remediable Service Statement (RSS).

When you left the Civil Service pension scheme you received a statement of your pension benefits. As a result of the 2015 Remedy ruling, when you claim your preserved pension, you will be given a choice of the benefits you wish to receive for the remedy period, 2015 to 2022. The RSS provides statements showing the pension benefits for both PCSPS and alpha.

In 2015 the Government introduced reforms to public service pensions and most civil servants were moved into a new scheme called ‘alpha’. In 2018, the Court of Appeal found that some of the rules put in place in 2015 were discriminatory on the basis of age. As a result, steps are being taken to remedy those 2015 reforms, making the pension scheme provisions equal for all members. This is called 2015 Remedy (McCloud). Further information on 2015 Remedy, can be found here.

You just need to read the pension benefits statements you were sent and tell us if you change your address or marital status via the member portal or by using the forms on the Civil Service Pensions website. If you wish to register for the portal please click here.

You don't need to do anything else now; this is for information only and represents the changes to your preserved benefits following the introduction of Remedy.

You'll make your choice when you claim your pension benefits.

As part of the Remedy, we want to ensure that affected members have a choice about the pension benefits for service within the Remedy period (01 April 2015 – 31 March 2022). Therefore, members will be given two options, which is known as Deferred Choice Underpin (DCU).

You don't need to do anything else now; this is for information only and represents the changes to your preserved benefits following the introduction of Remedy.

You'll make your choice when you claim your pension benefits.

Your choice will be between:

The Remediable Service Statement you were sent (made up of pension benefits statements), shows the current value of your preserved benefits in each scheme under each option.

Please note: If you left prior to 1 April 2022, there are no alpha benefits under option A.

Previous benefit statements produced were based on your pension scheme membership at the time of issue. Since October 2023 this may have changed and these statements show the up to date position, including your Deferred Choice Underpin (DCU) Options A and B, as at current date that would be payable from your Normal Pension Age.

You'd typically claim your pension when you reach your normal pension age.

Depending on your circumstances, you may be able to claim your pension before you reach your normal pension age, but the amount you receive would be reduced for early payment.

Reckonable service is the amount of time you served in Civil Service employment that counts towards your pension and is affected by several factors, such as:

This means the reckonable service that counts towards your pension could be lower than the total amount of time you served in your Civil Service employment. Further information about how changes in working patterns can impact your reckonable service can be found here.

Your reckonable service could also be impacted if you previously partially retired, retired from a previous period of service on ill-health grounds, transferred-in additional service from another pension provider, or opted to purchase additional years of service.

We can confirm that all of this has been factored into the calculation of your benefits.

Please note:

Qualifying service: Generally, this is the number of years and days you have been a member of the Scheme, and it qualifies you for certain benefits.

Reckonable service: The service that counts towards a pension.

If you are thinking of opting out of the Civil Service pension arrangements, remember that if you do, you will miss out on a range of valuable benefits for you and your family.

Your pension is an important part of your pay and reward package. As well as your pension contribution, your employer also pays a pension contribution on your behalf.

The Government has made it clear that all costs associated with the ‘2015 Remedy (McCloud)’ are ‘member costs’ and will be paid by the scheme.

COVID-19 has not caused any major delays to the project timeline.

The interest rates were determined by the Government’s three objectives, to firstly reflect the position members would have otherwise been in without the discrimination having occurred, secondly to recognise the circumstances of the award and thirdly to not unduly burden the taxpayer.

Further details on our rationale can be found in the letter exchanges between HMT and the Government Actuary.

Members do not need to go through a third party to claim McCloud remedy benefits. For the majority of members the choice will be straightforward and guidance will be provided by schemes to help in this decision, this guidance is free. Using a paid service will not mean that a member is given their choice any sooner or affect the options a member has.

Only a very small number of affected members are expected to require support from an independent financial advisor or accountant regarding their McCloud remedy. Where the small number of members with particularly complex circumstances seek advice, members will be able to submit evidence and if the scheme agrees that this advice was required, the member will be able to claim back the costs of this advice.

For classic members moved to alpha on 1 April 2022: they are now able to make a nomination in favour of more than one individual so they can update/ make a new nomination if they would like to. For further information head to the Death Benefit Nomination page.

Post rollback: Any members who have been rolled back into classic and had made a nomination for death benefit whilst in alpha (for more than one individual), this is valid for the Remedy period service and no action is required to update previous nominations. For further information head to the Death Benefit Nomination page.

Your IC RSS will only show you options in relation to the benefits you have built up after your original Partial Retirement award.

The Remedy (McCloud) legislative change affects benefits within the period 01/04/2015 to 31/03/2022. As your Partial Retirement was put into payment before 01/04/2015 they are unaffected by this change and your IC RSS will only show you options relating to benefits you’ve built up after this date.

Please be assured that your original Partial Retirement benefits will be unaffected by your option and will remain in payment. We will however carry forward your choice relating to your later Final After Partial award, and make the necessary adjustments as detailed by your choice.

Your Immediate Choice Remediable Service Statement (RSS) will provide an estimate of the current value of any untaken Remedy period benefits affected by your Remedy choice.

Your IC RSS will only show you options in relation to the benefits you have built up after your original Partial Retirement award.

The 2015 Remedy (McCloud) legislative change affects benefits within the period 01/04/2015 to 31/03/2022. As your Partial Retirement was put into payment before 01/04/2015 it is unaffected by this change and your IC RSS will only show you options relating to benefits you’ve built up after this date.

Please be assured that your original Partial Retirement benefits will be unaffected by your option and will remain in payment